How do you explain blockchain technology to someone who doesn t know it?

Blockchain technology has been a buzzword in recent years, but for many people, it still remains a mystery. Whether you’re an entrepreneur looking to integrate blockchain into your business or just someone curious about this revolutionary technology, understanding the basics of blockchain is essential. In this blog post, we’ll break down what blockchain is, how it works and its benefits, real-world applications and tips on how to get started with learning more about this game-changing technology. So grab a cup of coffee and let’s dive into the world of blockchain!

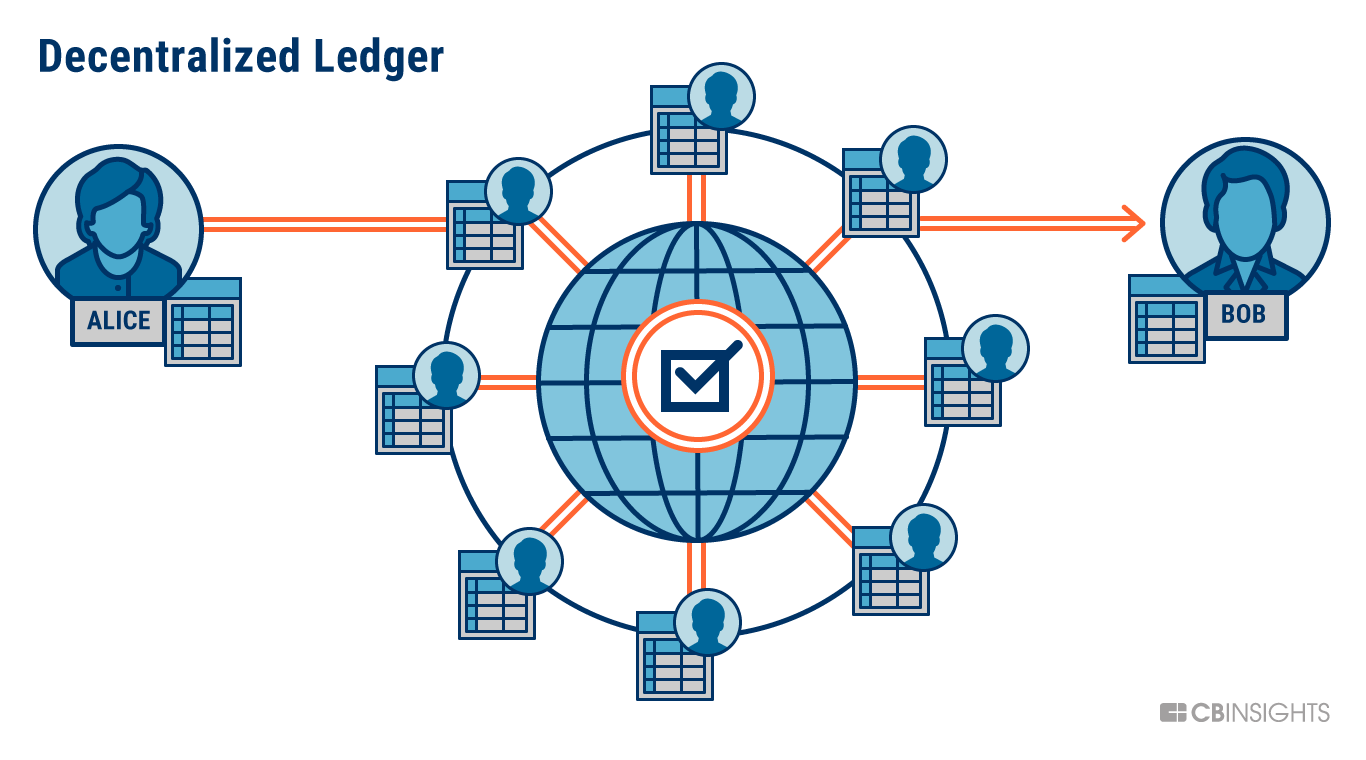

What is blockchain technology?

At its core, blockchain technology is a decentralized digital ledger that records transactions. This means it’s a database or spreadsheet of sorts, but instead of being stored on one central server, the data is spread across many different computers in a peer-to-peer network.

The beauty of blockchain lies in its immutability and transparency. Once a transaction has been recorded on the blockchain, it cannot be altered or deleted without consensus from the entire network. And because every participant in the network can view all transactions, there’s no need for intermediaries like banks to validate them.

Blockchain also uses cryptography to secure and authenticate transactions. Each block contains cryptographic code that links it to the previous block in the chain, creating an unbreakable “chain” of blocks that ensures security and trustworthiness.

Blockchain technology presents a new paradigm for securely storing and sharing information without relying on centralized authorities.

How does blockchain work?

Blockchain technology is a decentralized ledger that records transactions on a public digital platform. Each block contains information about the transaction, and once added to the chain, it cannot be altered or deleted.

The blockchain network relies on cryptography to secure and authenticate transactions between parties without the need for intermediaries such as banks or governments. It ensures that every participant in the network has access to an identical copy of the ledger, making it impossible for anyone to manipulate data.

Each block in the chain has its unique hash code containing important metadata such as timestamps and transaction details. The hash codes link each block together forming an immutable chain of blocks.

To add new blocks on this network requires consensus among participants through a process known as mining. Miners use specialized software to solve complex mathematical problems that verify new transactions before adding them to the blockchain.

Incentives are provided for miners who successfully validate transactions using cryptocurrency rewards like Bitcoin or Ethereum tokens, which encourages more people to participate in mining activities while maintaining security within the network.

Understanding how blockchain works provides insight into its potential applications across different sectors ranging from finance, supply chain management, healthcare systems and beyond.